Böll EU Brief

Trading partners? Europe's options against Trump's tariffs

Böll EU Brief 01/2025

Key findings:

-

The escalation of a tariff war between the EU and US would be mutually harmful. EU exports to the US would be slashed by half, with disproportionate impacts on Member States such as Ireland, Slovakia and Belgium.

-

The EU could negotiate a limited scope sectoral agreement with the US or deepen trade ties with its FTA partners. The latter strategy delivers larger GDP gains across all EU members, increases the EU’s global exports across a wider range of industries and reduces the bloc’s dependence on the US market.

-

To address the unequal distribution of economic burdens from a tariff war across EU members and sectors, the bloc should scale up instruments such as the Globalisation Adjustment Fund and deploy safeguards against trade diversion where necessary.

Since 20 January 2025, the United States (US) has adopted a dramatically different approach to its trade policy. Prior to this shift, average tariff rates imposed by the US towards most countries were as low as 2.6% on average. Under the current Trump administration, however, tariff rates as high as 50% across all imports have been announced and implemented towards certain countries, with hundreds of billions (USD) worth of imports from China, Canada and Mexico being subject, at least temporarily, to unprecedented new duties at the US border.

The European Union (EU) has consistently appeared to be ‘next in line’ for new tariffs, with the non-discriminatory tariffs on steel and aluminium being the first to directly impact the bloc. Additional tariffs targeting automobiles, pharmaceutical products and chemicals have since been threatened, while substantial reciprocal tariffs are also under consideration at the time of writing. This brief examines the potential effects of these increasingly likely scenarios and sketches possible EU responses.

To do so, this brief relies on simulation analyses conducted with the KITE model (Kiel Institute Trade Policy Evaluation),

Three strategic scenarios for the EU

- Scenario #1 – “Trade War”: US tariff escalation and EU retaliation. The US imposes 25% additional tariffs on all goods imported from the EU, similar to tariffs threatened against other key trading partners such as Canada and Mexico. In response, the EU implements retaliatory 25% tariff increases against US exports.

- Scenario #2 – “Trade Truce”: Limited bilateral tariff agreement with the US. Diplomatic efforts result in the EU successfully negotiating a sectoral trade deal with the US, granting mutual tariff elimination exclusively for industrial goods.

- Scenario #3 – “Trading partners”: The EU diversifies trade by deepening existing Free Trade Agreements (FTAs). Rather than depending on US political goodwill to negotiate a sectoral deal, the EU prioritises expanding trade ties with its FTA partners (e.g., Canada, Mexico, Japan, South Korea, Singapore, Vietnam). This involves modest reductions (5%) in non-tariff barriers, such as streamlined regulations, customs simplifications and reduced administrative burdens. The bloc continues to face elevated tariffs from the US.

This brief compares the economic effects of these scenarios in terms of changes in real Gross Domestic Product (GDP), total exports and exports specifically to the US. Analysing the impacts at the EU level, in Member States and at the sectoral level shows that a trade war has distributional implications in the Union and between sectors. However, it also shows that the EU has strategic options to reduce vulnerabilities and promote long-term economic resilience.

Economic impact of a trade war

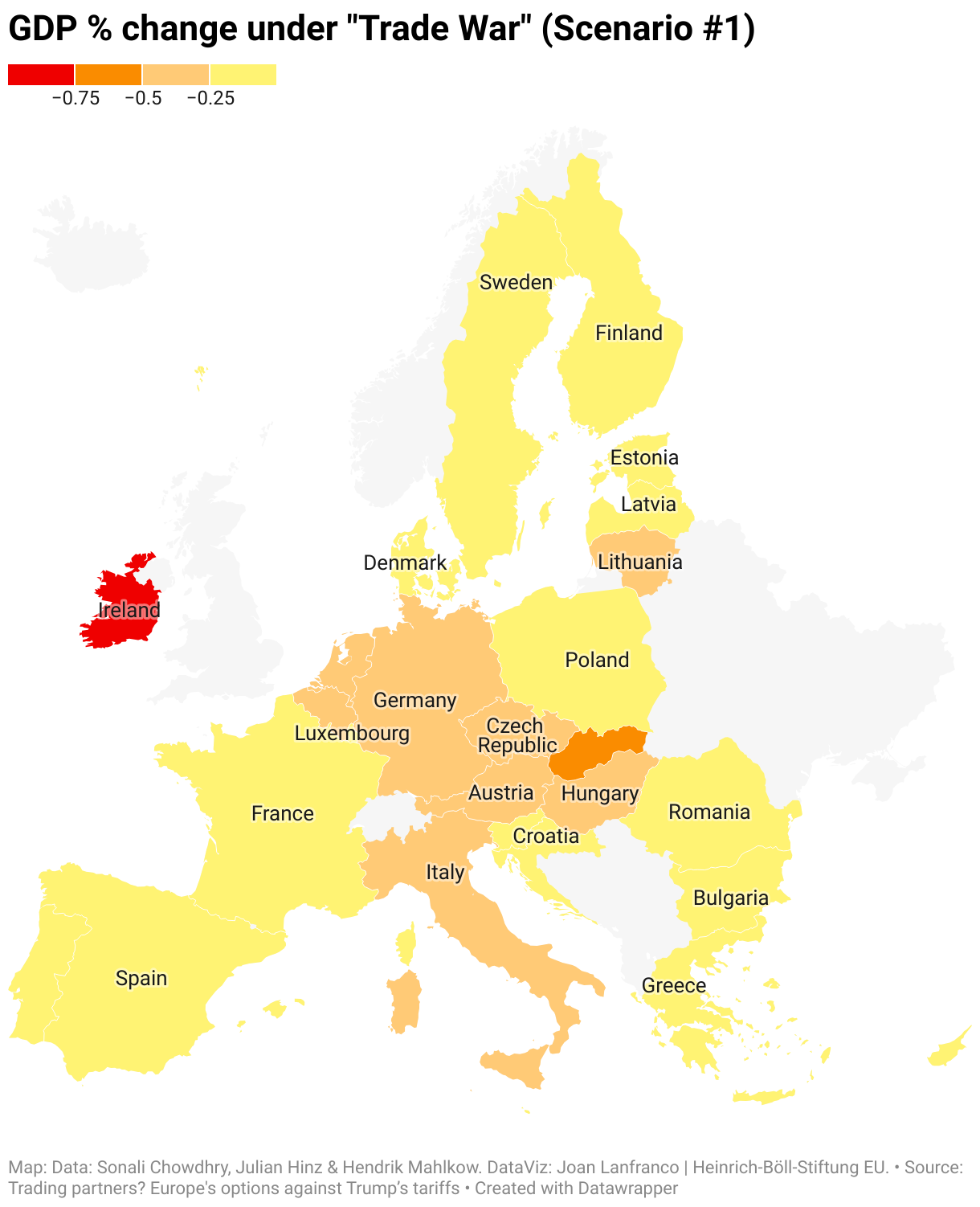

The trade war scenario (Scenario #1) reflects the most probable outcome if diplomatic efforts fail to ease trade tensions. Under this scenario, the EU’s real GDP drops by on average 0.25%, with one of the most marked contraction experienced by Germany (-0.32%). Given the density of input-output linkages between the EU and the US, the latter also experiences aggregate economic losses from the escalation of tariffs, with long-run GDP for the US contracting by 0.15%. Therefore, a trade war between the US and the EU is mutually harmful for these economies.

Several sectors in the EU take a substantial hit – with production declining in both goods and services sectors. Economically significant effects would be felt with regard to:

- Motor vehicles (EUR -42.9 billion, -4.1%)

- Pharmaceutical products (EUR -40.1 billion, -9.3%)

- Machinery (EUR -24.5 billion, -2.73%)

- Transport equipment (EUR -19.2 billion, -7.7%)

- Computer and electronic products (EUR -14.8 billion, -2.27%)

EU exports to the US would also face an unprecedented reduction of 50.5% (on average across members), with Slovakia (-74.1%), Lithuania (-61%) and Austria (-60.4%) experiencing the sharpest negative effects.

Truce or trade partners?

Given the economic costs of a prolonged trade war, the EU should invest diplomatic capital towards de-escalating tensions with the US (Scenario #2) and strengthen trade ties with other partners (Scenario #3) to cushion losses. In the trade deal scenario (Scenario #2), the EU enters into a limited scope sectoral agreement with the US with bilateral tariff elimination on industrial goods. The economic impact of this policy agreement is straightforward: as most goods traded between the US and the EU comprise industrial goods, eliminating tariffs will dial back the negative impact of imposed tariffs. The real GDP effects compared to the baseline without any new tariffs are close to zero across all EU Member States and the US.

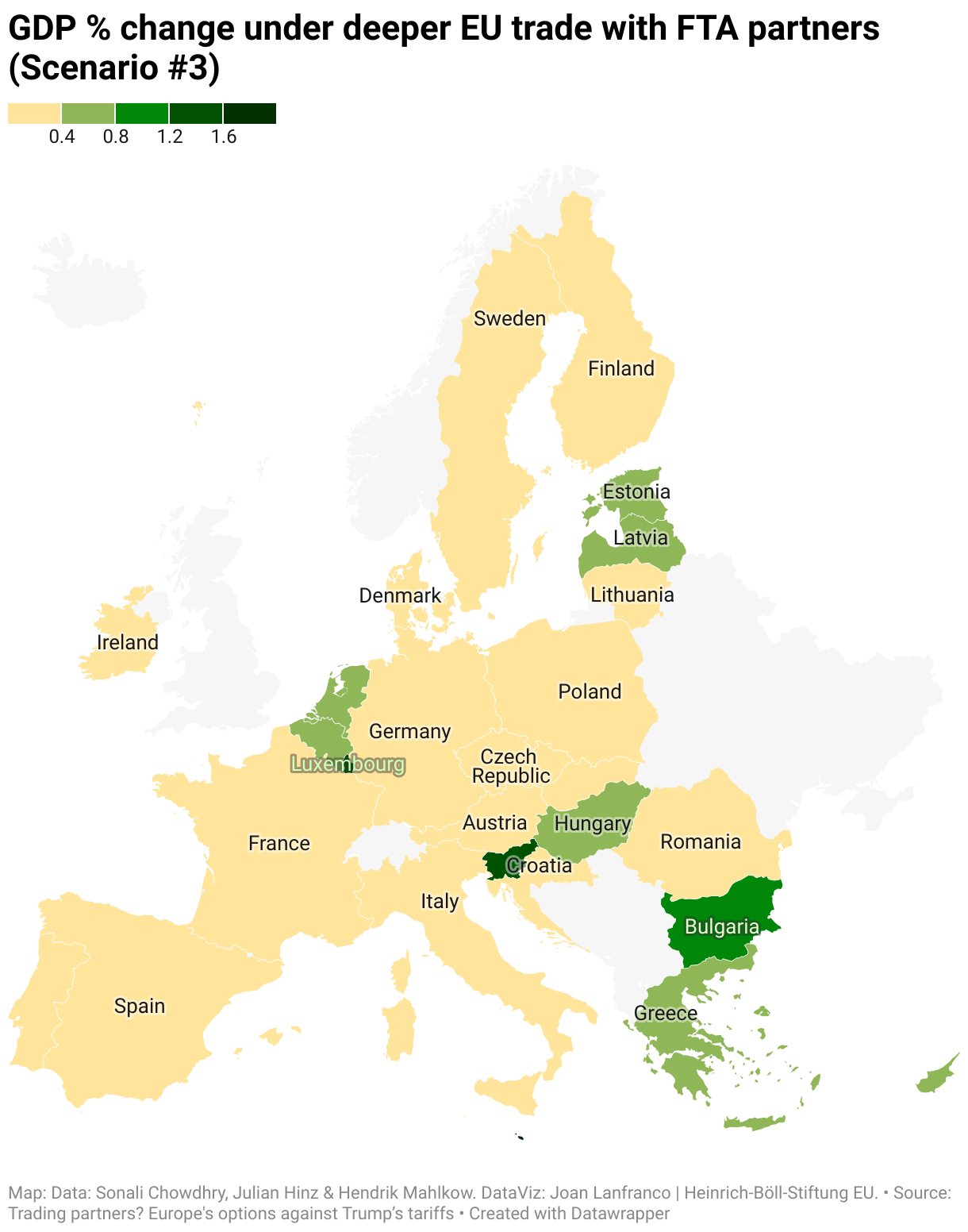

In the trading partners scenario (Scenario #3), the EU strengthens trade relations with its existing deep FTA partners through bilateral cuts in ‘non-tariff barriers’, which could encompass quota relaxations, regulatory harmonisation and reductions in red tape. This broadly reflects recent efforts by the EU, for example in modernising trade deals with Mexico and South Korea, and the pursuit of Clean Trade and Investment Partnerships with third countries to strengthen supply chains in clean technologies, energy and raw materials. Unlike Scenario #2, however, the EU in this case continues to face a trade war with additional 25% US tariffs – as in Scenario #1 – and maintains its retaliatory measures, opting for a broader trade diversification strategy over bilateral deals with the US.

Here, it is found that the EU experiences 0.28% GDP growth (EUR 61.3 billion, EUR 136 per capita) when the bloc deepens its existing FTA ties. This is driven by GDP increases across all EU members, such as for Germany (0.19%), Italy (0.17%), Spain (0.4%) and France (0.27%). Given broader market access across multiple trade partners, this growth is substantially higher in comparison to a trade deal (Scenario #2), where the EU partially liberalises trade with only the US through tariff elimination in industrial goods. Therefore, while both strategies offset the negative impact of rising US and retaliatory tariffs, deepening existing FTA ties proves significantly more beneficial for the EU. Comparing Scenarios #2 and #3, shows the powerful positive effects of reducing non-tariff barriers for growth, challenging the current emphasis on import duties as the primary instrument for trade policy.

At the sectoral level, Scenario #3 results in increased global exports for the EU across a wider range of industries, including service sectors such as:

- Business services (EUR 43.1 billion, 19.8%)

- Accommodation, food services (EUR 30.8 billion, 18.1%)

- Industrial goods like metals (EUR 29.4 billion, 48%)

- Motor vehicles (EUR 11.9 billion, 3.6%)

In contrast, Scenario #2 yields export gains that are concentrated in goods sectors, such as motor vehicles (EUR 12.2 billion, 3.7%), chemicals (EUR 7.5 billion, 3.83%) and leather products (EUR 4.1 billion, 11.1%).

The broader sectoral reach of Scenario #3 therefore generates economic opportunities for the EU that potentially benefit a larger pool of businesses, workers and regions across the bloc. Moreover, these scenarios have distinct implications for the geographic distribution of EU exports, and thus the bloc’s dependence on the US market in the long term. In Scenario #2, the EU increases its exports to the US, largely by diverting sales away from other markets. However, only in Scenario #3 does the EU truly ‘de-risk’ – reducing its reliance on US demand while expanding overall exports to the rest of the world.

Policy recommendations

The simulations show that a strategy of coordinating with other trade partners would not only neutralise the most severe risks posed by US tariff threats but also deliver tangible GDP gains across EU Member States over the long term. With a well-established network of trade deals, the EU is in a strong position to counterbalance future disruptions by deepening trade ties with its existing partners who may share similar concerns over declining trade with the US.

Further enhancing market access across these agreements would provide the EU with a substantial buffer against external trade volatility and an important foundation for economic growth that is less dependent on future shifts in US trade policy.

Such coordination between countries on trade policy has also proven to be effective against recent disruptions to the global trade regime, for instance in the case of tightening of sanctions measures against Russia. The positive effects of trade cooperation will only magnify if the EU were to expand its current network of FTAs. In this context, the bloc’s recent initiatives, such as to fast-track trade negotiations with India, are important steps in the right direction.

In addition to coordinating trade policy with other partners, the EU should prepare to counter the distributional effects of supply chain disruptions within the bloc. Without diplomatic solutions to avert the costs of a tariff war, several sectors in the EU are likely to face long-term production losses, though the severity will vary across industries. To mitigate this economic damage, the EU should consider targeted support for affected regions and workers, including temporary financial assistance through mechanisms such as the European Globalisation Adjustment Fund.

Furthermore, the European Commission should explore different mechanisms to finance such assistance. This could include revenues earned via retaliatory tariffs in addition to less volatile instruments that can ensure sufficient scale and plannability of funds.

Additionally, trade diversion from the US could lead to a surge in imports into the EU, as global suppliers seek alternative markets. This influx may necessitate temporary safeguards to prevent market distortions. At the same time, restricted access to the US may prompt some foreign suppliers to lower prices, presenting the EU with opportunities to secure more affordable inputs. Given the complex sector-specific dynamics, EU policy responses may need to be carefully tailored on an industry-by-industry basis.

In conclusion, while tariff retaliation against the US may offer the EU valuable leverage in current trade negotiations, it provides limited protection against the economic costs of trade uncertainty with the US over the long term. A bilateral agreement with the US can reduce some of this uncertainty but would simultaneously increase the EU’s dependence on the US. Recent examples of tariffs against Canada and Mexico also show that even existing FTAs with the US did not shield these countries from new tariffs. In contrast, deepening trade ties through a network of FTA partners can generate larger and more inclusive economic gains for the EU and would be a more advantageous strategy for promoting the bloc’s growth and resilience in the long run.

The views and opinions in this brief do not necessarily reflect those of the Heinrich-Böll-Stiftung European Union.