The year 2014 has been supposedly the most spectacular in Russian-Hungarian energy relations since the end of the Cold War. In January the Hungarian government signed an intergovernmental agreement with Rosatom about the construction of two new nuclear blocs worth of 12,5 billion euros. In early April Budapest also opened a 10 billion euros credit line, provided by the Russian government for the construction. In September, just a couple of days after Alexey Miller's meeting with Prime Minister Viktor Orbán and Gazprom's consent to the Hungarian request to supply gas into the country's storage, Budapest cut off reverse supplies to Ukraine. Despite the official reasoning, referring to technical bottlenecks, the move was allegedly taken at Russian request. Finally, in late October the CEO of the state-owned company MVM announced that Hungary may start the construction of the South Stream gas pipeline in the next half year.

This later move was taken despite the Commission's earlier declarations and notifications that the pipeline and the related agreements in their current form are not in line with the common regulations. Bulgaria has also attempted to start the construction of South Stream in spring 2014 and had to suspend it as a result of EC and US pressure. Austrian state-owned OMV signed the construction contract in June 2014, when the Crimea had already been annexed by Russia and intense fighting in the Donbass area had begun, triggering an intense wave of criticism in Brussels. Nonetheless, Budapest went even further and tried to violate, or at least by-pass the European law. What is more, the construction of the Hungarian section without its Bulgarian and Serbian counterparts is a non-sense. It may only cause another major tension in the already heavy-loaded Hungarian-EU relations. What is behind these events? How does Hungary look at South Stream?

Usually the transit countries' interest in the pipeline comes from two major sets of considerations: economic benefits and improved security of supply. The economic magnitude of the investment is relatively big especially in the smaller countries. Reportedly, in Bulgaria only the calculated transit fee revenue would have reached two percent of the country's GDP (in Hungary 0.2 percent was expected) . Apart from the one-time benefits of the construction, these countries can improve their bargaining positions regarding the Gazprom supply contracts, may get access to cheaper Russian or/and potentially even non-Russian (Azeri) gas supplies (if partial third party access would be granted). In the Hungarian case the synergy with the already existing, large-scale storage capacity (altogether more than 6 bcma, equal to 10 months imports) is a special additional factor. Since the gas delivered by South Stream would have to be “restructured” mainly for European winter supplies, Hungary may utilize its oversize storage system. It would be politically difficult for any government to ignore such an offer. This is particularly true for the incumbent Hungarian cabinet, that has set the foreign economic activity as an almost exclusive priority for diplomacy and MFA.

Strong pro-Russian signals

The second set of arguments comes from supply security considerations. After 2009, Hungary became the pioneer of sectoral adaptation to the emerging gas realities. Given the experience of the gas crisis, Hungary has started an ambitious interconnectivity programme, establishing connections with all its neighbours (except Slovenia). With the upcoming inauguration of the Slovakian-Hungarian pipeline, Hungary would be theoretically capable of importing all of its gas from westwards. This means the fulfilment of the “N-1” criteria, an important EU gas security benchmark for crisis situations. Coupled with the positive changes on the West-European markets, emerging hubs and hub-pricing, Hungary today imports more gas from the Austrian direction than through Ukraine. These efforts were supposed to give a good deal of relaxation in the Hungarian-Russian gas relations, improving the bargaining position of the former. Today the sectoral “hardware” seems to be optimized and a reasonable integration to the European market has been implemented.

Despite these developments the Hungarian sectoral “software” has been sending strong pro-Russian signals recently. One reason for this is the controversial record of regional diversification efforts: many interconnectors stand empty and lead to “nowhere”, in the neighbouring countries the network lacks investments. The grand-diversification project, the Nabucco-pipeline, potentially capable of bringing Azeri and other Middle Eastern gas to the region, failed in 2012. Despite its loud criticism of European gas policies, Gazprom has shown a good deal of adaptation to the new market realities. Consequently, apart from some smaller hubs (like Baumgarten) Russian gas is still the cheapest option in the region. Mediterranean LNG, imports from Western European (Dutch, Belgium or UK) hubs are not competitive with Gazprom's sources.

Furthermore, due to the Ukrainian economic situation and military conflict, the geopolitics of the Ukrainian transit has deteriorated tremendously in 2014. Today a more severe gas crisis is almost the order of the day, a likely outcome for any upcoming winter. Parallely, the EU-Russian energy relations are in freefall, the sides becoming less and less capable of managing their interdependence. Putin's cancellation of the South Stream construction can be easily interpreted as a strong signal, that if Europe does not cooperate in the management of transit problems, it will have to do it alone and take all the responsibility. A message, which cannot be ignored in the CEE region.

Gaining votes by cutting prices

All these trends contradict to the region's original interests. The Central Eastern European (CEE) countries would favour a diversification process parallel to a gradual and managed deconstruction of Russian dependencies. In contrast to these expectations, they get very weak and expensive diversification options, turmoil in Ukraine and a rapidly deteriorating EU-Russian gas relationship. This forms an inconvenient and unwelcome constraint of choice for CEE capitals. Not surprisingly, for most of these countries South Stream seemed to be a way-out from this situation and they hoped for a compromise at the EU-Russia level. It was not their fault, that they have to remain “on the Ukrainian pipeline” in the foreseeable future.

Nonetheless, in Hungary a third major factor played a likely pivotal role in the cabinet's pro-Russian attitude: the use of utility, especially gas and electricity rate cuts as an electoral instrument. The conservative government has decreased utility prices by more than 25 percent during the 2013-14 electoral campaign. This policy turned out to be a “Wunderwaffe” in terms of popular support: Fidesz's electoral base had increased from 1.3 million people in 2012 to roughly 2.1 million voters at the April 2014 elections. Thus the issue of energy prices are of utmost importance for Viktor Orbán. However, given the political taboo of price raises and the huge tensions around financing the losses in the state-owned energy company MVM, the doors for a bigger Russian leverage are open. The easiest way to financially sustain such a populist system is to get price short-term concessions from the biggest supplier.

It is highly likely, that Orbán's newborn Russia-friendship is not totally independent from these considerations. He made a U-turn compared to his past policies and signed a nuclear deal in Moscow just three months before the elections. What could prompt him to do so in such a sensitive moment? Maybe Gazprom's price reductions in October 2013 and February 2014 played a role in this. Gazprom showed readiness to inject its gas into the Hungarian storage capacities instead of the state-owned MVM, that obviously lacked the money. Understandably Gazprom could easily have also asked for some favours, perhaps even a cut-off of the Ukrainian reverse flow. In the light of this potentially broad agenda, it would be difficult to decide to what extent has the Hungarian position on South Stream its roots in a policy context, or whether it is only just another bargaining chip in the bilateral relations.

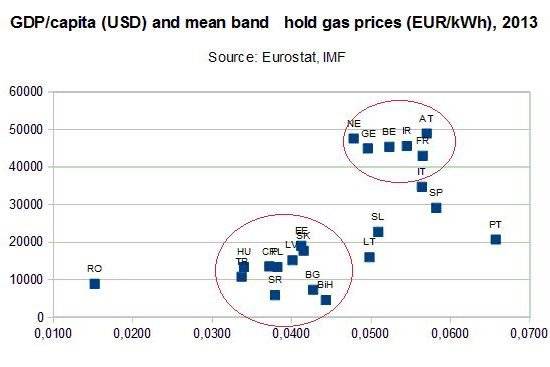

The Hungarian example is a good demonstration of the complex nature of CEE energy policies. Two major issues dominate the regional energy policy patterns: supply security considerations, namely the Russian dependence and the problem of social affordability. Even if there is a lot of talk about the former, the later has grown increasingly significant in parallel to the growing oil and gas prices since the early 2000s. As it is shown in the Graph below, CEE end-user gas prices are usually much lower than in most of the Western-European states. Despite higher regional import prices and capital costs, these countries sell natural gas at cheaper prices to their people, primarily because of their lower GDP/capita, social affordability reasons. Even with these lower price levels, energy often constitutes a higher share of CEE household expenditure than in Western Europe.

![]() Photo: Eurostat, IMF. All rights reserved.

Photo: Eurostat, IMF. All rights reserved.

{kind=link}

The social and political sensitivity around energy prices has far-reaching implications for the regional policy frameworks. These countries cannot afford large-scale and expensive diversification or energy saving programmes, if not from external funding. As examples in the Czech Republic, Bulgaria or even in Poland show, the probability of policy failure at these projects are bigger, the political implications are more serious in the region. In Bulgaria even the government fell due to attempted electricity price raises in 2013. Poland built its LNG-terminal almost exclusively from EU-funding, but had to limit its utilization due to high LNG-import prices. Social affordability especially at high oil price levels is an overarching constraint for energy policies, ranging from diversification efforts to climate policies. Furthermore, if energy populism is present, it also may become a matter of political survival, an invitation letter for Russian influence.

{kind=link}