[Click here to download article as PDF]

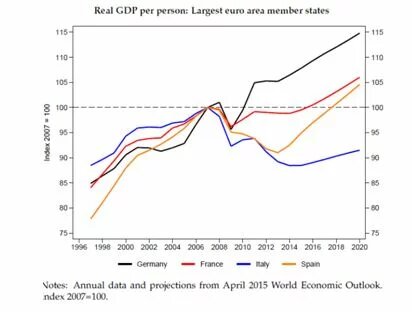

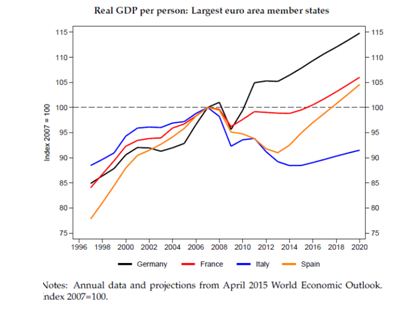

More than eight years since the outbreak of the global crisis and five years into the eurozone crisis the Union looks widely divided. Between 2010 and 2014, debtor and creditor countries alike have implemented ‘a massive contractionary shock – equal to four percentage points of the monetary union’s economy. The GIIPS [Greece, Ireland, Italy, Portugal and Spain] accounted for 48% of the fiscal swing, even though they accounted for only a third of EZ GDP .. EZ core nations decided that they too had to embrace fiscal rectitude. As the monetary union’s largest economy, tightening by Germany accounted for 32% of the Eurozone’s overall fiscal tightening. France’s austerity amounted to 13% of the EZ total.’ (CEPR 2015, p. 10-11). As a result of these austerity policies, only a few of the EZ nations have recovered their pre-crisis growth and employment rates (fig. 1), while socio-economic conditions in the periphery have worsened dramatically. With households, corporations and governments simultaneously reducing expenditure, income and production dropped and unemployment soared, with youth and long-term unemployment and inactivity rates at record heights. The destruction of physical, human and social capital occurred in this period will take years to redress. Meanwhile, the euro area is churning out the world's largest current account surplus in value terms (approximately 3.0% of GDP in 2015) (fig. 2). The bulk of it is accounted for by Germany (7.9% of GDP) and the Netherlands (10.6%), but also the former deficit countries are now recording balanced or surplus positions, reflecting the steep fall of their production and imports. In a context of enduring low growth in the core and deep recession in the periphery, the persistence of very high surpluses in core countries, far from denoting virtue, denounces ill-judged policies [1].

Several years of harsh austerity have also taken their toll in terms of inequality and poverty, cancelling a significant part of the gains in living standards achieved by low-income households over the past 20 years. Welfare provisions have been cut everywhere: the European Union’s ambitious targets for combating poverty and achieving social inclusion are self-delusive because of the constraints faced by member states in the periphery, that hold responsibility for implementation and are no longer in a position to ensure even a minimum level of social inclusion [2]. All over Europe, the economic malaise is feeding extremist views, nationalistic, anti-euro and anti-EU rhetoric.

While Greece and the other periphery countries are (barely) kept afloat by the ECB’s quantitative easing (QE), new financial shocks cannot be assumed away. In fact, QE alone is at best ineffective, at worst conducive to new bubbles. Thus, stagnation is slowly spreading to the core, threatening France and the Nordic countries. With the rest of the eurozone in enduring recession and the international economy (China and emerging economies) losing pace, also the mighty German export engine may splutter [3], dragging the eastern European countries with it.

How did we get here? The proximate causes of the crisis

The common interpretation of the causes of the crisis is that it was triggered by excessive foreign indebtedness by peripheral countries: huge capital flows from the core to the periphery, facilitated by the monetary union and its regulatory framework [4]. Although, as it is by now agreed, the crisis was not led by fiscal profligacy (with the exception of Greece) [5], when the crisis broke out, the ‘sudden stop’ in cross-border lending, the EZ institutions and the governments’ short-sighted choices combined in triggering a vicious cycle between banks and their government which amplified and spread the crisis (CEPR 2015).

More importantly, however, the common currency eliminated the mechanisms that an individual country could normally rely on to defuse a crisis, such as monetary and exchange rate policy, without replacing them with other adjustment mechanisms at the supranational level. With monetary independence (a lender of last resort) and devaluation forgone, the euro-denominated foreign borrowing was akin to foreign currency debt. However, as noted by Orphanides (2015, p. 3), ‘in contrast to situations facing crisis-stricken countries elsewhere, the design and implementation of an IMF program for Greece (and subsequently for other euro area member states) effectively became subject to the approval of each of the other governments of the euro area. The result was the domination of the decision making process by competing and conflicting financial and political interests among member states of the euro area. Rather than work together towards containing total crisis-related losses, politics led some governments to focus on shifting losses to others.’ Since restructuring the debt of crisis-stricken nations like Greece would have hurt the banks in creditor nations [6], and possibly spread a contagion, a readjustment programme with harsh conditions attached was preferred instead. Fiscal tightening pushed the Greek economy into a deep recession, deteriorating the public balance despite the balancing efforts, triggering a financial panic that soon engulfed the other debtor nations. The ECB’s commitment ‘to save the euro’ in September 2012, on condition of persevering in fiscal consolidation and structural reforms, succeeded in calming the financial markets, but synchronised fiscal austerity reignite the crisis (double dip).’ The result was unfortunate but predictable: massive destruction in some member states, and a considerably higher total cost for Europe as a whole.’ (Orphanides 2015, p. 3).

Eventually, in early 2015 the ECB implemented a policy of ‘quantitative easing’, that is, injecting large amounts of money into the economy. One year into this policy, however, we must conclude that, while effective in depreciating the euro, thus providing some relief from exports, QE has been ineffective in making credit available to firms, stimulating investment and expenditure and kick-starting the EZ economy. To be effective, monetary policy should be seconded by fiscal policy, but there is no corresponding party to the Central Bank, no fiscal policy at the EU level responsible for the EU-wide aggregate demand, while, at the country level, indebted nations’ fiscal policy is severely constrained by the Stability Pact. Thus, the excess liquidity which is created overflows into interest rates, the euro exchange rate, and Target2 balances.

To conclude, the creation of a Monetary Union without a fiscal and political union led to ignore the problems of the transition to a full integration and the crucial issue of who should eventually pay the costs of this incompleteness. As it is argued in the next sections, this means that it ignored the problems originating from the different stages of development of its member states. The crisis, mistakenly interpreted as a standard fiscal/balance of payments problem, would have required institutional corrections coherent with these basic flaws.

Alternative exits

The discussion on how to steer the EZ economy out of its present quagmire has focused on two alternatives: expansion of internal demand of ‘core’ countries (Germany) or internal devaluation (wage flexibility) for the deficit (Southern European) countries. In a paper written with Andrea Ginzburg and Gianluigi Nocella (Simonazzi et al. 2013), we argued that the first solution is politically unfeasible and probably insufficient, and the second is economically unsound, socially unfeasible and ultimately counter-productive. And, indeed, it is the latter that has been carried out, until now (German GDP growth for 2015 is estimated at 1.6%, hardly a stellar growth).

It is doubtful, however, whether fiscal expansion in Europe’s core economies would suffice to boost sustained growth in the periphery, and for two reasons. First, an increase in German public investment would certainly stimulate that country’s domestic demand in the short run and also durably raise its output. Its effects on the peripheral countries’ GDP would depend on a number of factors, among which the stance of monetary policy (Blanchard et al 2014) and the import content of the (direct and indirect) increase in German demand. However, the regional distribution of the spillovers associated with such a programme can prove quite different, for they are in fact much smaller for the southern European countries than for other European countries. In a recent study, Elekdag and Muir (2014) have estimated that a one percent increase in government investment would increase German real GDP by 1.05 percent, other (central) euro-area countries’ GDP by 0.30 and the peripheral countries’ GDP by 0.20; the impact on current accounts is similarly differentiated: -0.57, 0.12 and 0.05 percent respectively.

More importantly, however, we must take into consideration that these spillover effects will reflect the core country’s process of investment and restructuring as determined by its choices and priorities, not what is needed to sustain the autonomous development of the partner countries. What is good for Germany is not necessarily good for them. That is, an undifferentiated expansion of the core’s internal demand, though helpful, will not be up to address the deep and growing eurozone development inequalities. The peripheral countries need public investment targeted to their specific needs, capable to envision and encourage the direction of change and innovation that better ensures attainment of autonomous development. Only in this way can the increase in the peripheral countries’ income prove sustainable in the long-run. An independent strategic policy of industrial development, however, calls into question the institutional construction of the eurozone, the fiscal compact and the monetary policy rules.

Given the institutional constraints, there is little hope that this ‘third’ alternative may prevail, at least in the short term. In spite of increasing consensus on the perverse effects of austerity policies implemented in recession (Blanchard and Leigh, 2013), ‘readjustment’ policies are still relying solely on the ‘positive’ effects of internal devaluations – a relative decline in domestic prices and wages, compared to the rest of the euro area – to regain competitiveness [7]. This is not only a slow and much painful process, but it is also vain, as concerns its primary objective, that is, export promotion: as observed by Marie Diron, senior vice president and economist at the ratings agency Moody’s, ‘What drives exports really is demand. Cheap doesn’t help if the demand isn’t there’ (Ewing 2015). Then, the question is if demand is there and whether peripheral countries’ productive base is adequate, in quantitative and qualitative terms, to respond effectively to external demand, the only dynamic demand component, given the deflationary effect of the Stability Pact on internal demand.

How did we get here? The structural causes of the crisis [8]

A longer-term perspective helps us to better assess this issue and the limitations embedded in the adjustment policies that have been imposed upon the debtor countries of the periphery. These policies are short-sighted in two respects: they do not help the economies to recover from the crisis in the short-term (the perverse effect of synchronised austerity) and, by ignoring the structural causes of the crisis – that is, the peculiar problems faced by countries situated at different stages of development – they fail to adopt the policies required to ensure a long term sustainability. In fact, the institutions of the EMU are based on the premise that each country starts from the same level playing field except for ‘less modern’ (‘anti-competition’) institutions and individual values and attitudes. The implicit assumption of this approach is that an austerity regime, associated with institutions close to those assumed to be prevailing in ‘core’ countries, would create in the periphery the ‘right’ environment for a persistently low cost of capital and ‘thus’ for a sustained investment flow. This flow would automatically originate especially from external sources (Foreign Direct Investment) [9].

This simplistic assumption, and its related forecast, is falsified by the post war European economic development experience. The analysis of the main phases of the European countries’ development since the second post-war provides evidence of wide differences in the productive structures of the countries of the centre and the southern periphery of Europe at the start of the Europeanisation process. This entailed an asymmetric capacity of countries at different levels of development to adjust to external shocks. In fact, the process of development, which consists in moving up towards more complex, less ubiquitous products (Hausmann and Hidalgo 2011), is far from linear. Since it occurs through diversification into products ‘near’ to those that are already successfully produced and exported, a country’s ability to add new products to its production depends on having many nearby products and many capabilities used in other, potentially more distant, products. Countries with a low diversity of capabilities can get stuck in ‘quiescence traps’, that make catching up more difficult. The existence of discontinuities in the product space and the need to develop and coordinate those capabilities that growth industries demand prove a formidable obstacle to the process of development. That’s why government policy is called to coordinate the dispersed actions of firms, help them identify new opportunities for differentiation and upgrading, and contribute in developing the capabilities that are needed for the production of more complex products.

As argued in Berger (2013, p.13), in Germany (but this is true also of regional clusters in other countries, e.g., the Italian industrial districts) proximity to suppliers with diverse capabilities allows to create new businesses not through start-ups – the US model – but through the transformation of old capabilities and their reapplication, repurposing and commercialisation. The crisis of the 1970s, associated with the saturation of the main mass consumer goods in the advanced countries and the start of globalisation, led to a deep transformation in demand, production and competition. Demand for substitution and quality competition (vertical diversification) favoured the passage to markets dominated by a product-led competition. These changes marked a profound break in the history of the relations between the centre and the periphery of Europe. The ‘centre’ succeeds in strengthening its ability to stay in the market thanks to processes of 'creative destruction’ and reconstruction, undertaken in the crisis with the support of industrial policies. The restructuring of the core deeply affects also the countries of the periphery which, in the reorganisation of their economies, struggle to adapt to the new environment (dominated by deflation and quality competition). Faced with a situation that would have called to innovate the state’s capabilities in order to facilitate selective guidance and reorientation of investment to contrast a rapidly weakening economic structure, they adopt instead across the board liberalisation policies, implementing what might be called a 'plain destruction' of their capabilities to create new products, market niches and markets.

‘Market fundamentalism’ … the fallacious proposition that markets in general, and financial markets in particular, are capable of regulating themselves and therefore do not need public regulation’ is ‘the most important policy failures underlying this crisis’ (Padoa Schioppa 2011, p. 319-20). The author (former Italian Minister of Economy and Finance and former member of the Executive Board of the ECB) argues that by the end of the 1970s this ‘radical idea’ conquers ‘universities, trading rooms, newspaper editorial boards, think tanks, central banks, treasury departments and parliamentary committees ... Policy makers became not only non interventionists but also active deregulators.’

In the 1980’s, also as a consequence of their policies, peripheral countries’ growth fell behind: the crisis associated with deregulation opens a gap in aggregate demand, eventually filled by welfare and construction expenditure. This ‘premature deindustrialisation’ – restructuring without industrialisation – exposed the peripheral countries, even before the formation of the Monetary Union, to stunted growth and persistent fragility with respect to external changes.

The slow growth of the euro area did not sustain the capacity of southern European countries to achieve a sufficient level of diversification and specialisation of their productive structures; or it even contributed to worsening it (as seems to be the case of southern Italy). Conversely, the increasing integration of the central and eastern European economies within the supply chain of German industry speeded up their process of diversification-cum-specialisation. The eastward integration of German industry, combined with the persistent containment of internal demand of the major economies of the euro area, has gone hand in hand with an impoverishment of the productive matrix of those southern regions less connected with Germany and, more generally, with the general redirection of trade flows (Simonazzi et al. 2013, p. 664).

It follows from this analysis that austerity measures are not going at the root of the development and debt sustainability problems of southern European countries, which rest in their lacking a sufficiently broad and differentiated productive structure. Given the differences in the level of development of the various EU countries, and their different capacity to cope with change, fiscal policy should have been assigned two complementary targets: a redistributive and compensative function, and the role of actively promoting – through investment – the removal of development bottlenecks and renewal of the productive base. Lacking this guidance, the forces protecting and freezing the status quo from the point of view of both institutions and productive specialisation thus prevailed. ‘The way was open for a kind of bank-led ‘privatized Keynesianism’ (which in some countries took the form of a construction and consumption bubble) that concealed – until the outbreak of the global crisis – the existence in the European peripheral countries of a demand-and-supply constraint on development.’ (ibid., p. 657)

Industrial policy

The policy implication of this approach is the assignment of a strategic importance to investment guidance by the State and industrial policies geared to diversify, innovate and strengthen in a long period perspective the economic structures of peripheral countries. These same policies are currently implemented ‘under the radar’, that is in a discreet way, in the core countries, but are wholly excluded from the list of measures that the European institutions and the IMF recommend to peripheral countries in order to satisfy conditionality clauses (for these institutions, ‘structural reforms’ are simply another name for ‘deregulation measures’ of the economy). In the mainstream approach the problem of development is mostly to achieve static efficiency: to better allocate resources by countering the market failures caused by monopolies, asymmetric information, and externalities.

More recently ‘there has been a revival of the role that industrial policy can play. In this context, the issue is no longer the whether of industrial policy, but rather the how’ (Landesman 2015; quoting Rodrik 2008). Also the European Commission has finally acknowledged the need for a European policy of public investment, but its conception of industrial policy is still confined within the narrow limits of acting as catalyst of private capital for innovative projects. The much publicised Juncker plan [10] – using a small amount of public money to lever private capital, thereby encouraging enterprise investment, growth and job creation – is manifestly inadequate for the aim of kick-starting growth in the European Union and helping the peripheral countries towards sustainable long-term convergence. Leaving aside the trifling amount of money appropriated and the uncertainty about the effective ability to attract a significant portion of private investment, its conception of industrial policy still places faith in the capacity of the market to ensure convergence while reflecting scepticism about the ability of governments to manage the economy [11]. This is still very far from a view of development as the result of the complex web of linkages connecting different institutions in a dynamic interaction, with the government acting as long-term ‘strategic organiser’ rather than short-term ‘market optimiser’ (Mazzucato 2013). The attention paid to linking the inter-related elements of the productive structure makes the difference between capability-driven industrial policy and government direct assistance to business, and, consequently, creation of innovativeness, on the one hand, and creation of dependency on the other (Best 2013).

Most important, a strategic industrial policy is not simply about developing competitive advantage for growth; it is also about characterising social needs that are consistent with sustainable prosperity. Modern capitalism faces a number of great societal challenges: population ageing, youth unemployment, rising inequality, migration flows, climate change. ‘These challenges have created a new agenda for innovation and growth policy that require policymakers to “think big” about what kind of technologies and socio-economic policies can fulfil visionary ambitions to make growth more smart, inclusive and sustainable.’ (Mazzucato 2014) The latter aim involves shaping sector strategies to provide for material and social consumption infrastructures. To play this ‘strategic role’ the state must succeed in attracting the talent, expertise and intelligence needed to envision and address contemporary challenges.

Thus, simply investing in infrastructure is not the goal; it is necessary to align production and consumption infrastructures in ways that foster socially rational long-term growth (Best 2013). Positive complementarities between equity and efficiency in the knowledge-based economy suggest that 'investing in people’ and targeting inequality more closely could respond to the urgent need of creating employment while favouring innovation and long-term sustainability. Higher employment is an indispensable prerequisite for the long-term sustainability of an inclusive system, while an increase in the supply of skilled human capital needs to be matched by an increase in the supply of quality jobs. Capacitating public services can yield better long-term results than the neo-liberal deregulation of labour markets, which works by lowering labour costs and providing incentives for the unemployed to take on poorly paid jobs. Accommodating critical life-course transitions reduces the probability of being trapped into inactivity and welfare dependency. This calls into question the whole adjustment agenda of the ECB and the EC. Austerity policies, constraining the spending capacity of government, force to cut social investment, while structural reforms, as interpreted solely as favouring more ‘flexible’ labour markets, undermine long-term growth.

Concluding remarks

We argued that the crisis was mistakenly interpreted as a standard fiscal/balance of payments problem, while it originated from the incomplete nature of the European institutions and the disregard for the consequences of differences in the various members’ stages of development. The creation of a Monetary Union without a fiscal and political union led to ignore the problems of the transition to a full integration and the crucial issue of who should eventually pay the costs of this incompleteness. Joining the euro, member states relinquished national crisis management tools without any supra-national governance in their place. The ideological pre-conception that market are self-equilibrating through price-competition has justified disastrous policies of internal devaluation in the belief that an austerity regime, associated with institutions close to those assumed to be prevailing in ‘core’ countries, would create in the periphery the ‘right’ environment for resuming growth. The assumption of an equal level playing field has led to disregard the need for industrial policies geared to cope with the peculiar problems faced by countries situated at different stages of development.

From these premises, it follows the proposal of a radical change of policies, a long-term plan aimed at activating the interactions between firms and institutions and the interdependencies between aggregate demand and the supply of products and capabilities. Several suggestions have been advanced: from a policy of public investment financed by eurobonds, a strategy of converting a part of external debt obligations of peripheral countries in a strategic plan of investments (with a public-private partnership) (Mazzucato 2013), to the consolidation of national government debts (budgetary union). All of these proposals stress the benefits accruing to society from the possibility to finance much needed public investment almost for free. A common fiscal authority that issues debt in a currency under its control – it is argued - would prevent destabilising capital movements within the eurozone and protect the Member States from being forced into default by financial markets. This would restore the balance of power in favour of the sovereign and against the financial markets (De Grauwe 2015). Finally, favouring the establishment of a sustainable development path these policies could also create the foundation for the repayment of the loans associated with the investments.

There is still very little hope for a radical change of policies along these lines: they would require changing the EZ rules. The willingness to move in the direction of a budgetary and political union in Europe today is non-existent. This will not only continue to make the eurozone a fragile institution, but justifies Orphanides’ desolated conclusion that ‘In its current form, the euro poses a threat to the European project.'(2015, p.2)

[1] It is of little comfort to read in the Alert Mechanism Report 2016 (European Commission 2015a): ‘Once oil prices rise again, domestic demand strengthens, the effect of the lower euro fades away and export growth slows, the trade balance surpluses of the euro area and the EU should stop widening and eventually decline slightly in 2017.’

[2] https://www.bertelsmannstiftung.de/fileadmin/files/user_upload/Study_EZ_SIM_Europe_Reformbarometer_2015.pdf

[3] “The BRICS region has contributed roughly one-fifth to Germany’s export growth since the crisis, with value added figures likely to be even higher… this regional concentration of German export growth limits the exportability of Germany’s success and at the same time puts it on shifting grounds”(Unger 2015, p. 9).

[4] Orphanides (2015, p. 11) observes: ‘The regulatory framework that had been created by the governments treated all euro area sovereigns as zero-risk-weight assets, from a capital requirement perspective, and exempted them from regulations regarding large exposures.’ The author suggests that these rules might have induced the financial markets to assume away the country risk.

[5] Spain and Ireland had one of the lowest public debt to GDP ratios, and Italy had lowered its public debt by ten percentage points of GDP; by contrasts Germany and France allowed their debt ratios to rise above the 60% Maastricht limit (CEPR 2015, p. 5).

[6] Orphanides reports a ‘startling and controversial’ statement given by the former governor of the Bundesbank, Karl Otto Pöhl, in an interview published by Spiegel on May 18, 2010, just one week after the Troika program was decided: ‘It was about protecting German banks, but especially the French banks, from debt write offs’ (quoted in Reuter, 2010).

[7] The IMF itself, one of the first, within the mainstream, to warn against the perverse effects of implementing austerity policies in recession, has mixed feelings. A recent IMF publication (IMF 2015) concludes that wage moderation in the crisis-hit economies is deflationary, but, by reducing long-term interest rates, monetary policy can play a crucial role in mitigating the appreciable negative spillovers of this moderation on other euro area economies. That is, ‘Beggar-thy-neighbour’ wages policy is indeed deflationary but quantitative easing can work to offset its devastating effects (Janssen 2015). As in Blanchard et al. (2014), this conclusion relies on the existence of a relation between interest rates and investment which has dubious theoretical (and empirical) validity.

[8] This part draws on Simonazzi and Ginzburg (2015).

[9] See, for instance, the European Commission’s last Annual Growth Survey (2015b).

[10] Initiated in 2014, the European Fund for Strategic Investments (EFSI) – better known as the ‘Juncker Investment Plan’ – is too strong on ambition. It ‘earmarked’ almost €315bn to finance European sustainable growth aimed at activating private funds for a total investment volume estimated at €1300bn in key sectors such as infrastructure, energy, innovation, education and SMEs. ‘However, only €21bn from the EU budget and the European Investment Bank will go to replenish the EFSI as a financial guarantee’, while it is doubtful that private funds will produce the multiplier effect expected from the confidence boost (Bercault and Yeretzian, 2015).

[11] The Italian Banking Insurance and Finance Federation (2014, p.4) favourably assessed prospects for the plan on the grounds that ‘It is market-oriented, and directed at promoting investment that is financed in the market, or through the market, minimizing therefore the risk of wasteful public “white elephants”.’

{kind=link}

{kind=link}