Blog

After 21 consecutive quarters of positive evolution of the eurozone, one might think that the euro crisis is permanently over. But the eurozone has been playing with fire for too long. It has imposed policies with large economic and social costs, while ignoring fundamental and long lasting weaknesses in the design of the euro architecture.

The summer lull and the synchronised economic growth that is finally observed in the eurozone, with the eurozone as a whole growing for 21 consecutive quarters since the second quarter of 2013 may have led many to think that the euro crisis is permanently behind us and that the past and impending reforms have enhanced the resilience of the eurozone to shocks. Greece just exited ‘successfully’ its third bailout programme on 20 August. Thus, for many observers in northern eurozone member states, following years of uninterrupted economic growth and lower unemployment rates, there is little understanding if the Italian government submits a 2019 budget proposal foreseeing a deficit that exceeds 3% of GDP. Such fiscal stances are seen as endangering the hard-won budget deficit consolidation achieved through fiscal discipline, i.e., through the eurozone austerity strategy.

However, a recent IMF Staff Country Report on Greece provides an elucidating assessment of the situation in Greece and includes two figures that hopefully might help dispel what can perhaps be considered, in the best case, as wishful thinking, in the worst case, as propaganda.

The IMF report provides an update of its debt sustainability analysis (DSA) of Greece’s public debt, to reflect the more recent debt relief measures by Eurozone authorities, granted just prior to Greece’s exit as a kind of ‘Godspeed’ present.

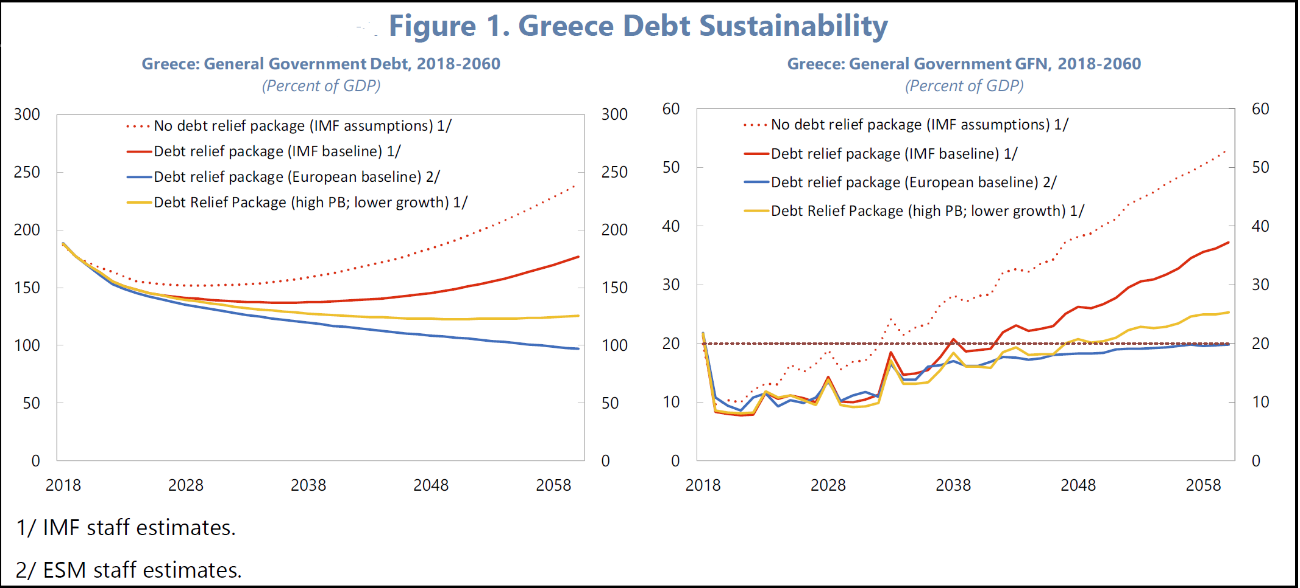

Source: IMF Staff Country Report 31 July 2018, p. 45

The new debt relief measures approved by the Eurogroup (IMF baseline) improve Greece’s public debt trajectory slightly. Greece’s public debt now starts rising again after 2038 (before, it started rising after 2030), and by 2060 the IMF estimates that Greece’s debt will be around its present levels. Thus, according to the IMF, Greece´s public debt is still not on a sustainable trajectory. Greece’s public debt is also not sustainable according to a second criterion, the level of debt gross refinancing needs relative to GDP, arising from the need to repay public debt that comes due in each year, with outlays exceeding 20% of GDP after 2040, a level considered unsustainable.

Interestingly, the DSA of the eurozone authorities, prepared by the European Stability Mechanism according to the IMF, suggests that Greece’s public debt is barely sustainable on the two above criteria, with public debt levels falling to just under 100% of GDP after 42 years (i.e., by 2060) and gross financing needs of nearly but just below 20% of GDP after 2050.

Clearly, the Greek crisis is not really over, and the ‘wheeling and dealing’ that has been accomplished by eurozone policy makers is just about enough to put Greece back on track for the next decade, if Greece is lucky.

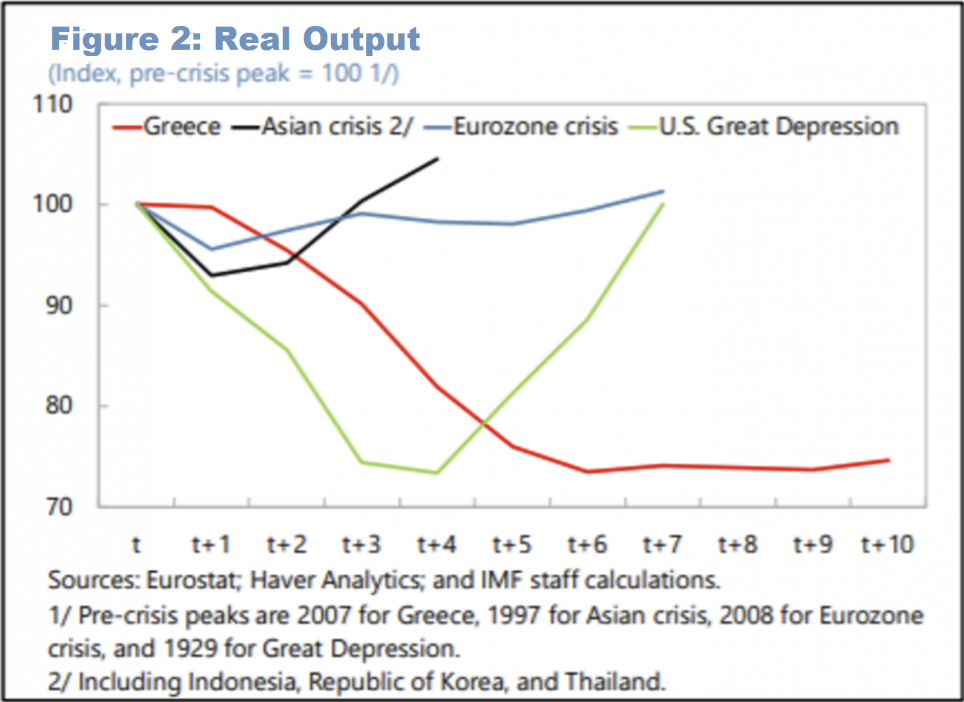

Source: IMF Staff Country Report 31 July 2018, p. 5

Figure 2 suggests that the eurozone recovery from the euro crisis has been dismal and uneven. The eurozone, though not experiencing as deep a recession, needed 7 years to surpass its pre-crisis peak output, nearly the same time the US needed to recover from the Great Depression. In 2017 the eurozone real output was just 5.7% above its 2008 peak, an average growth rate of 0.6% yearly since then. However, Greece’s real economic output in 2017 was 25.3% below its peak of 2007 and its economic depression is, relative to the size of its economy, as deep as the US during the Great Depression. However, it has lasted much longer (10 vs. 4 years) and there seems to be no end in sight.

But if Greece was, so to say, the unfortunate and unwilling ‘trial balloon’ of the eurozone crisis response policy, the eurozone defining test seems to be waiting in the near future, in how it will respond to Italy’s ‘Secular Stagnation’.

Italy’s economic performance since the adoption of the euro has been very poor. Ghiaccé [1] points out that Italy is experiencing its ‘worst peacetime economic crisis since 1861. Italy’s real output in 2017 was 5.4% below its peak of 2008. Its unemployment rate is very high, particularly among its youth (30.8% in July 2018), despite the massive emigration of 1.5 million Italians, foremost young cohorts, in the last decade. In 2017, its public debt and public deficit were 131.8% of GDP (2.3 trillion euro) and 2.3% of GDP, respectively. And the interest rate on Italy’s 10-year public debt hovers presently around 3.2%. The contrast on these macroeconomic indicators with member states such as Germany could hardly be greater. It is as if Germany and Italy were living in two entirely different (macroeconomic) worlds. Nonetheless, Italy’s macroeconomic position is relatively stable as it has a current account surplus of 2.8% of GDP and its net international investment position, while still negative, has improved markedly in recent years.

The negotiations between Italy and the eurozone authorities will follow a carefully arranged choreography. Pressure versus a little accommodation here and there. The Eurozone Fiscal Compact Treaty rules will be creatively interpreted, once again for a large eurozone member state. The status quo is likely to prevail for a few more years. Nobody really wants to rock the boat. Every eurozone member state has too much to lose if a shipwreck occurs with all its dramatic consequences, of unimaginable proportions.

But the eurozone has been playing with fire for too long. It has managed for nearly two decades to administratively control the economic policy making of entire countries, imposing misguided policies with large economic and social costs, while ignoring fundamental and long lasting weaknesses in the design of the euro architecture.

Eurozone authorities have thus far been able to pull an incredible feat: with several of its member states in economic stagnation for over a decade and embroiled in the World’s largest peacetime balance of payments crisis, the authorities have kept the euro going, with relatively minor changes to the existing framework, while putting in place additional policy constraints.

Italy, in the present, needs fiscal space and policy instruments to promote domestic growth, the development of domestic industries, and to promote employment and productivity growth. The Eurozone Fiscal Compact Treaty, competition policy, monetary policy and Italy’s high public debt essentially prevent any meaningful government macroeconomic stabilisation policy to do as such.

A compromise will likely be reached whereby Italy will be allowed to increase public spending and/or public investment by a few tenths of percentage point of GDP. It will, essentially, be ‘much ado about nothing’.

The main risk, of course, is that the new populist Italian government will not ‘play ball as usual’ this time. The new Italian government includes knowledgeable macroeconomists in important positions, who believe that the current path is unsustainable, a grave risk to Italian sovereignty, and who fear the consequences of the euro flaws to Italy’s future as a nation. Further, due to the architecture of the euro, a singularity – which, by definition, is almost impossible to forecast precisely - is always around the corner.

For the time being, the ECB largely determines fiscal consolidation performance of member states, not only through the control of the eurozone monetary policy (and interest rates) but also through the supervision (and the resolution or liquidation) of the eurozone significant banks.

If interest rates on Italian public debt continue to rise, the Italian budget deficit will worsen and in accordance with the Fiscal Compact Treaty rules, the European Commission will likely recommend the applications of fines and other penalties.

The current monetary policy framework, if strictly adhered to, also dictates that, if at some point Italian debt is downgraded from investment grade to non-investment grade (‘junk’) by all four main credit rating agencies, the Eurosystem should cease accepting Italian debt as collateral in the Eurosystem refinancing operations, unless Italy asked for a bailout and committed to a fiscal adjustment program negotiated, in practice, with the Eurogroup.

Thus, the prospect of a downgrade of Italy’s public debt would trigger an additional round of selling of Italian public debt and lead to much higher interest rates.

The above scenario is not inconceivable and indeed something similar occurred recently. In January 2017, the little known Canadian credit rating agency DBRS downgraded Italy’s debt from A (low) to BBB (high), in a decision that was in part a consequence of Italy’s constitutional referendum in the autumn of 2016. Due to the Eurosystem collateral rules (see Table 2 of guideline (EU) 2016/65 of the ECB), this resulted in eurozone banks having to provide significantly more collateral to obtain liquidity from the Eurosystem, making Italian debt less attractive and more costly.

If Italy were under the threat of downgrade to non-investment status by all four main credit rating agencies, the negotiations for a bailout would be fraught with political tension. It is also possible that Italy’s government might refuse to ask for a bailout, to ‘make a stand’, so to say.

Thus, a credit downgrade by all four rating agencies might lead to a default of Italy on its public debt.

This is the worst-case scenario, very unlikely in the present, for which, however, the main eurozone member state chancelleries are hurriedly preparing, in a discreet contingency planning exercise.

But this clear and present danger to the survival of the eurozone, always hanging over our heads, like a Sword of Damocles, is no way to run the World’s second largest economy!

[1] Giacché, V. (2017) “The Real Cause of the Italian Bank Bailouts and Euro Banking Troubles”. Institute for New Economic Thinking, 19 July.

of the ECB")

{kind=link}

{kind=link}